Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Companies in Austria are extending credit to a growing share of buyers while keeping payment terms short. The market appears stable at first glance, but liquidity pressures are mounting beneath the surface. Late payments tie up cash and strain operations, prompting many businesses to proactively use a multi-layered approach to credit risk management to protect financial health. This balance of opportunity and caution defines the market’s strength.

48% of B2B sales are now transacted on credit in Austria, broadly in line with the Western European average. The upward trend, particularly evident in manufacturing, is driven by more buyers turning to trade credit to cope with tighter financing and rising costs. While this carries some risk, it mirrors trends across the region. Payment policy remains tight, with rapid settlement seen as essential for working capital management. Most suppliers keep payment terms within a 30 day credit window. This preference for short settlement cycles is stronger than in Western Europe. Longer payment terms remain an exception in Austria and appear most common among SMEs in construction.

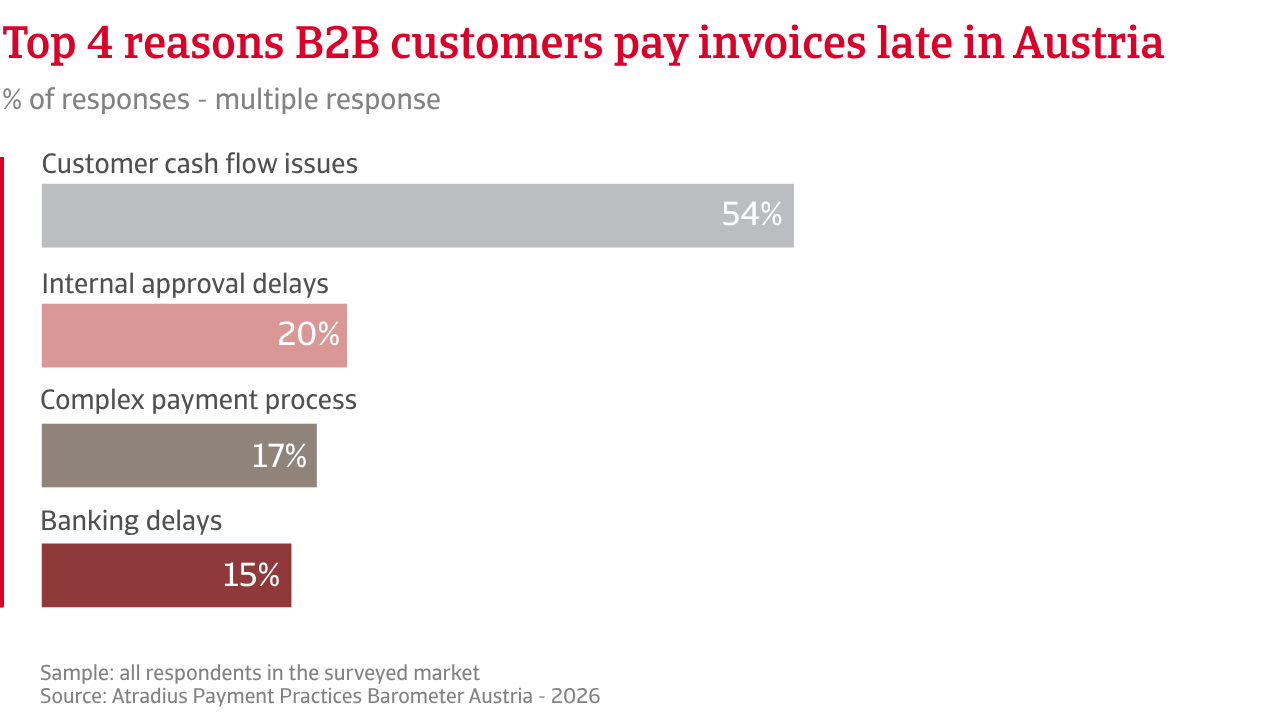

On the surface, Austria’s focus on consistent payment patterns suggests a healthy and disciplined credit environment. However, the underlying pressure is more significant than the headline stability implies. More companies in Austria (84%) than across Western Europe (77%) report being impacted by B2B late payments during the past months. A larger share of Austrian companies than across the region, mainly in trade, also report delays sitting in a range of 20% to 40% of B2B invoices impacted. This ties up a meaningful share of cash and places greater pressure on liquidity. The figures for Days Sales Outstanding (DSO) reveal slower collections, which results in more pronounced working capital constraints for suppliers in Austria than in Western Europe. Bad debts affecting an average of 2% of B2B invoiced turnover of Austrian suppliers are higher than across the region. In response, firms in Austria bridge liquidity gaps with external financing, including demand for supplier credit, and are more likely to do so than Western European peers.

Austrian firms manage customer payment risk through comparatively stronger financial protection and more formal enforcement than the Western European average. They rely more heavily on credit insurance and bad debt reserves, reflecting a focus on containing losses through a multi-layered approach. Western European firms, comparatively, place greater emphasis on active credit management, process automation, and customer diversification. This points to a more process‑driven and portfolio‑based approach, aimed at managing payment risk while maintaining commercial relationships within the current unsettled trading environment.

The upward trend in B2B sales on credit, particularly evident in manufacturing, is driven by more buyers turning to trade credit to cope with tighter financing and rising costs.

Our survey finds there is widespread concern among companies in Austria about insolvency trends for the year ahead due to the unsettled economic landscape. This is broadly in line with sentiment across Western Europe, with half of Austrian firms anticipating that insolvencies will remain elevated. The rest expect either further increases or hold no firm view. This signals concern over ongoing financial stress in the market rather than a short-lived shock, and of an operating environment where underlying weaknesses have not yet eased. Sector patterns reinforce this outlook. The concentration of insolvencies provides a clear view of where stress is expected to remain acute in the short term. The services and construction sectors will be the main drivers of Austria’s insolvency trend due to volume driven pressure in services and structural vulnerability in construction.

These issues feed directly into profitability. Austrian businesses anticipate stronger margin pressure than their Western European peers and they expect continued margin compression rather than a sharp contraction. Persistent cost pressures will remain central. Operating costs are expected to stay high, and firms will continue to struggle to pass these fully on to customers. Demand softness narrows pricing power, particularly for firms serving consumer markets.

As profitability seems likely to remain constrained across key sectors there is great uncertainty about the outlook for B2B payment behaviour. Cost pressures, sector fragility, and residual payment risks, however, continue to weigh more heavily in Austria than elsewhere. Manufacturing highlights this vulnerability as a sector facing high input costs, weak export demand, and ongoing supply chain risk. Even if collections improve, these constraints will limit the extent to which manufacturers can turn better payment behaviour into stronger margins.

Companies in Austria also continue to closely monitor the short-term risk landscape. Economic slowdown, ongoing cost pressures, and geopolitical turmoil remain the top risks expected to disrupt B2B payments in the short term. These risks, combined with concentrated insolvencies and uneven sector performance, reinforce the need for structured risk management. Against this backdrop, Austrian firms acknowledge that protecting cash flow, strengthening operational resilience, and maintaining discipline in credit decisions will remain essential as the economic and trading environment continues to be unsettled and largely unpredictable.

For a full overview of the 2026 survey results for Austria and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis