Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Bulgaria’s macroeconomic outlook points to steady but slowing growth, supported by domestic demand but constrained by inflation, weaker confidence, and external uncertainty. While price pressures have eased, they continue to weigh on costs and liquidity. Insolvency risks remain contained but are edging higher, reflecting tighter financial conditions and uneven sector performance. The result is a more fragile operating environment.

Within this context, trade credit remains central. More than half of business-to-business (B2B) sales are conducted on credit, above the CEE average, with SMEs in manufacturing most active. Credit use is rising across the region, though Bulgarian firms are offering it more cautiously. This reflects a need to support sales while protecting liquidity in a still uncertain demand environment.

This caution is evident in payment terms. Bulgarian firms prefer short term, with more companies than in CEE setting due dates within 30 days from invoicing. Longer terms are less common and largely limited to smaller manufacturers. Some flexibility is emerging to support customer relationships, but this also raises exposure to delays if not carefully managed.

Late payment remains widespread, with around 80% of firms reporting overdue invoices, slightly below the regional level. The key difference lies in distribution. Bulgaria shows a more mixed picture, with more firms reporting both very low and very high levels of overdue receivables. This points to strong discipline in part of the market, but acute financial stress in others. Payment timing reinforces this contrast. Overdue invoices are more likely to be paid beyond one month past due than in CEE, while longer delays remain contained. However, this has led to longer collection times particularly in specific segments, notably construction.

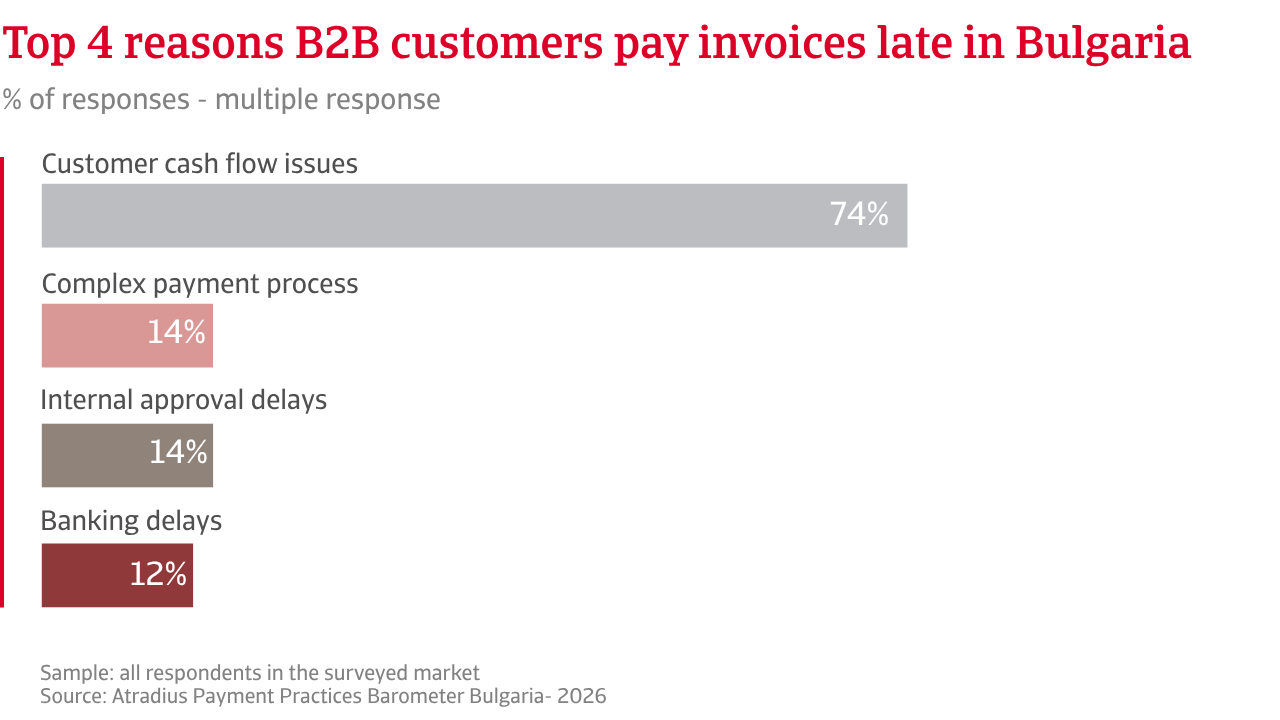

The drivers of delayed payments point clearly to liquidity stress. Bulgarian firms cite customer financial pressure more often than peers in CEE, while operational issues play a smaller role. Delays are therefore rooted in financial constraints rather than operational inefficiency.

Bad debt trends remain contained. There is some increase, consistent with slower settlements, but less pronounced than in CEE. Losses are mainly driven by disputes and customer inactivity, suggesting risks are still being managed before turning into write-offs.

As survey data show, Bulgarian businesses absorb the impact of payment risk on working capital mainly through greater reliance on external financing, reported by over a third of businesses. Fewer firms report operational challenges, suggesting some control over day-to-day liquidity. However, greater dependence on funding reduces financial flexibility and signals underlying pressure. A significant number of companies also rely on internal reserves to absorb potential losses, while the use of credit insurance remains markedly lower than in CEE.

Trade credit remains central. More than half of business-to-business (B2B) sales are conducted on credit, above the CEE average, with SMEs in manufacturing most active.

Bulgaria’s business outlook mains cautious. Significantly more companies than across the wider CEE region expect little improvement in B2B payment behaviour in the coming months. Those anticipating change believe it will come from financially stronger customers rather than a broad improvement in market conditions.

Across both CEE and Bulgaria, around half of businesses expect insolvencies to rise in the coming months, while about one third believe the current levels will remain high. This reinforces the view, particularly among Bulgarian companies, that financial stress will continue for long. The stronger pessimism in Bulgaria points to greater concern about the fragility of the business environment, which underlines the need for careful credit risk monitoring, even as payment behaviour may show limited signs of stabilisation.

Profit expectations remain mixed. In Bulgaria, nearly one quarter of businesses expect margins to decline, confirming ongoing pressure on profitability. Compared with the wider CEE region, where fewer companies anticipate contraction, Bulgaria appears more exposed to downside risk. Across the region, uncertainty remains the most widespread sentiment, yet the balance of risk is clearly less favourable in the Bulgarian market.

When asked about the main risks that could disrupt B2B payment behaviour in the coming months, Bulgarian companies point to a broad range of challenges. Inflation, economic slowdown and geopolitical instability are all expected to continue weighing heavily on payment performance. Elevated concern about fraud risk also highlights underlying operational vulnerabilities. In contrast, firms across CEE focus more narrowly on macroeconomic pressures, with economic slowdown and inflation remaining the dominant risks.

Overall, the outlook suggests Bulgaria faces a more complex and exposed risk environment. While businesses across the region deal with macroeconomic pressure, companies in Bulgaria face a wider mix of challenges. This makes them more sensitive to shocks and keeps their outlook more cautious.

For a full overview of the 2026 survey results for Bulgaria, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis