Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Tighter access to bank credit, driven by heightened risk perceptions amid rising geopolitical uncertainty, has prompted Italian firms to shift financing along the supply chain, with the result that the share of B2B sales made on credit has increased in recent months, broadly in line with trends across Western Europe. Italian firms now conduct nearly two thirds of B2B sales on credit, well above the just over half regional average. This higher reliance on trade credit increases exposure to customer payment risk, which explains why companies remain focused on balancing support for demand with the need to protect liquidity.

Payment terms point to a slower payment culture than in Western Europe. Only two in five Italian firms set terms within a 30-day credit window, well below the regional share. Far more businesses offer longer terms, reflecting a reliance on extended credit to sustain customer relationships and support business continuity, although this raises pressure on working capital and increases liquidity risk. Customer payment behaviour appears currently under pressure, as Italian firm more often report delayed payments from business customers than their regional peers. Although an average of one quarter of invoices is past due, consistent with the regional average, settlement takes significantly longer in Italy. Fewer invoices are paid within one month past due, and delays extend well beyond the regional benchmark. This highlights a more persistent delay cycle in Italy than regionally.

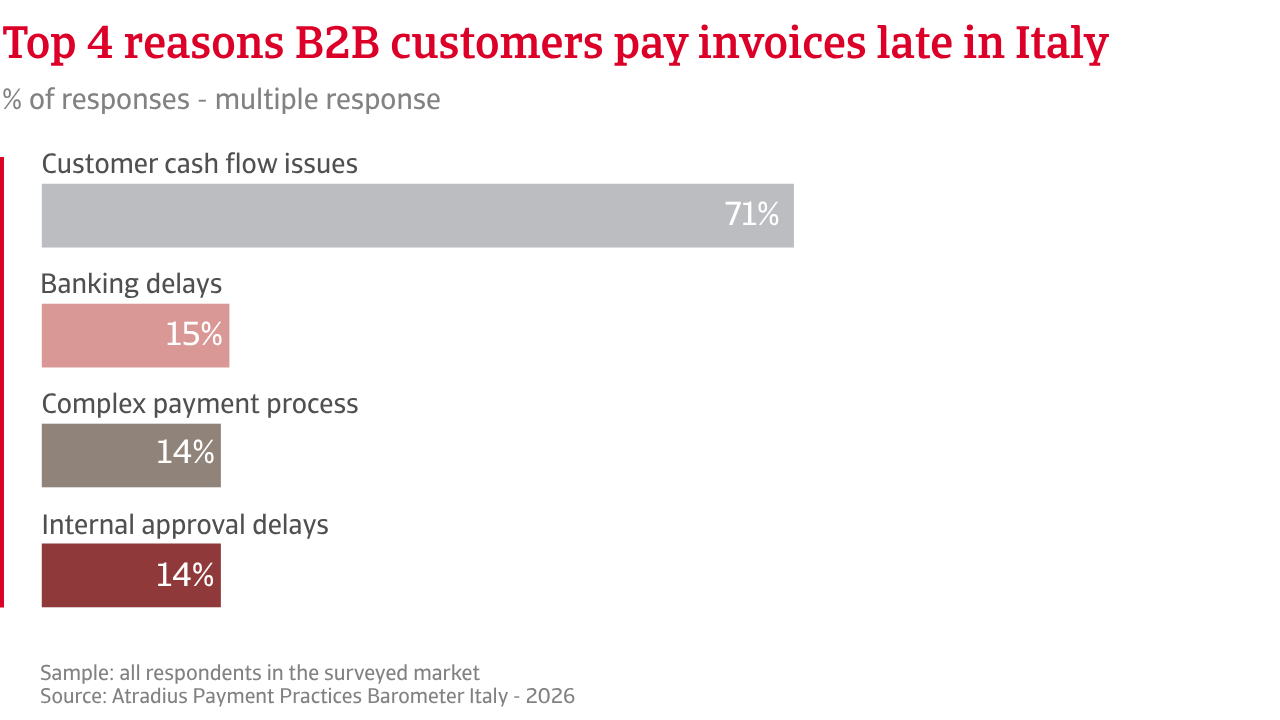

Liquidity stress is the main reason why business customers delay payments. Far more companies in Italy than in Western Europe say late payments are due to customer cash flow stress. This leads to longer collection cycles and ties up working capital. Shifts in Days Sales Outstanding (DSO) confirm this, pointing to a structurally weaker payment behaviour in Italy than regionally. Credit losses also reflect this landscape. A larger share of companies in Italy than across Western Europe reports losses in the 5%-10% range, a level which markedly erodes profit margins and weakens the liquidity position.

The main impact of customer payment risk on working capital reported by Italian companies is reduced cash available for operations, as delayed payments tie up cash and limit operational flexibility, while regional peers more often highlight impacts such as tighter financial planning and greater reliance on external financing. Italian and Western European companies appear to manage customer payment risk in different ways. Italian firms focus more on staying close to their customers, closely monitoring payment behaviour, renegotiating payment terms when needed, and transferring risk to insurance. Companies in Western Europe are comparatively more likely to manage risk by building financial buffers, using different types of financing, and improving internal processes such as automation and payment systems.

A larger share of companies in Italy than across Western Europe reports losses in the 5%-10% range, a level which markedly erodes profit margins and weakens the liquidity position.

Italy’s economic outlook remains subdued, with weak demand, inflationary pressures, and insolvency levels continuing to weigh on business confidence and liquidity conditions. Against this backdrop, companies show a cautious view of short-term shifts in B2B payment behaviour.

Far more companies in Italy than in Western Europe do not expect any meaningful change in already slow B2B payment timings. Those that do expect a shift are more likely to anticipate deterioration rather than improvement, which reflects ongoing concern about customer solvency and liquidity. Overall sentiment appears more negative in Italy than in Western Europe.

A similar pattern emerges in expectations for insolvencies. More Italian businesses than their regional peers do not anticipate any short-term change in insolvency levels, which are expected to remain high as rising input costs, elevated interest rates, and tighter financing conditions continue to weigh on business finances. Among firms expecting a shift, the majority foresee an increase in insolvency levels rather than a decline, while some remain uncertain.

Profit expectations reinforce this outlook. Italian firms largely expect margins to remain broadly stable, at modest levels, or decline in the short term, rather than increase. Western European companies, by contrast, show greater optimism about a recovery in profitability. The gap highlights the more constrained position of Italian businesses, which continue to face pressure from high costs, weak demand, and tighter liquidity.

Risk expectations follow a similar pattern. Italian companies that expect B2B payment behaviour to deteriorate in the coming months express concern over ongoing economic uncertainty, customer liquidity stress, and rising costs. There is also concern about the impact of ongoing geopolitical tensions and energy market volatility on businesses.

Italian firms worry that these challenges could significantly disrupt intercompany payments, increasing the risk that business customers may struggle to pay. Although Western European companies face similar macroeconomic pressures, they appear relatively less concerned, suggesting that the outlook remains more fragile in Italy than in Western Europe.

For a full overview of the 2026 survey results for Italy and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis