Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

High inflation and weak household demand are slowing consumption in Romania, pointing to softer growth in the months ahead. Investment is expected to remain the main driver of activity, but overall momentum is likely to stay fragile due to tighter financing conditions and uneven performance across sectors.

Within this context, trade credit remains widely used. Over half of business-to-business (B2B) sales in Romania take place on credit, markedly above the CEE average. SMEs in trade and services are the most active users. Credit sales have increased recently across the region, but Romanian firms are expanding more cautiously than their CEE peers. This reflects the need to support demand while protecting liquidity in an uncertain environment.

Payment terms are broadly in line with the regional pattern, with most invoices due within 60 days. Terms beyond this are less common in Romania, showing tighter control over risk exposure. In recent months, there has been a gradual shift towards longer terms, slightly stronger than in the wider region. Romanian firms are offering more flexibility to stay competitive and maintain customer relationships, though this raises the risk of delayed payments.

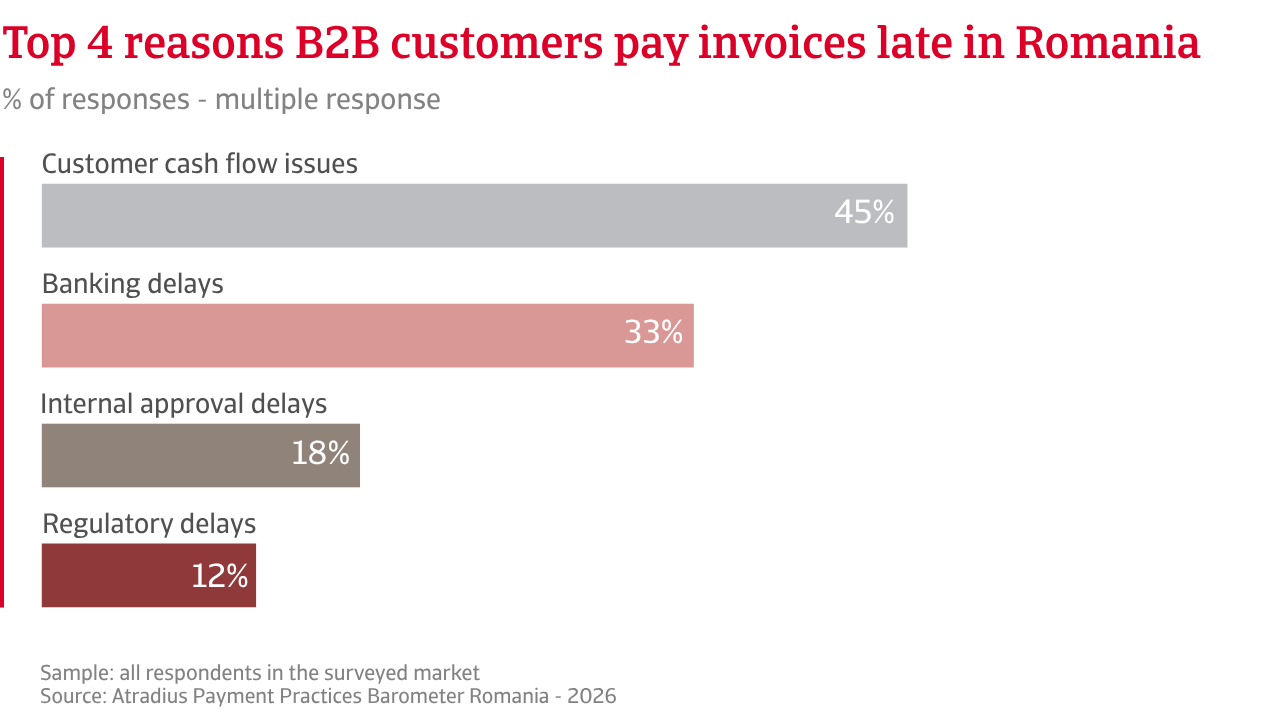

Late payments are widespread, with around 83% of Romanian businesses reporting overdue invoices, in line with the CEE average. However, the pattern is more uneven. While some firms manage receivables well, others face significant delays, leading to greater unpredictability in payment performance.

Settlement takes longer than in CEE. A smaller share of invoices is paid within 30 days past due, while more fall into the 31-to-60-day range. Delays beyond 60 days are broadly in line with the regional average. This suggests that, while extreme delays are not more common, overall payment timeliness is under pressure.

Days Sales Outstanding (DSO) confirms this trend, with collection periods becoming longer and putting pressure on cash flow. Romanian businesses also report a sharper rise in bad debt than the regional average. This is often linked to ageing receivables, pointing to growing difficulty in recovering payments.

The impact on working capital is clear. Most Romanian firms report insufficient liquidity for operations and respond by delaying payments to suppliers, a behaviour reported by over one-third of companies and far above the regional average.

Romanian businesses take a more hands-on approach to managing payment risk. They rely more on cash terms, advance payments, and active credit management. Diversifying the customer base is also more common. At the same time, they make less use of risk transfer tools. Credit insurance remains less widely used, while softer measures such as incentives or shorter payment terms are less common.

High inflation and weak household demand are slowing consumption in Romania, pointing to softer growth in the months ahead. Investment is expected to remain the main driver of activity, but overall momentum is likely to stay fragile.

Expectations for B2B payment behaviour remain muted in Romania, and confidence is weaker than across the wider CEE region. Businesses remain cautious about the speed and sustainability of any change. This reflects ongoing pressure on cash flow, as well as heightened uncertainty around the economic outlook. As a result, companies are not yet expecting a meaningful improvement in payment discipline and remain alert to the risk of delays.

Just over half expect customer insolvency risk to rise, a share broadly in line with, but slightly more uncertain than, the regional benchmark. Among the remaining respondents, around one quarter expect insolvencies to remain at current levels, while a similar share expresses no clear view. This distribution points to limited visibility and a more fragile perception of customer solvency.

These expectations match survey data. Slower collections and higher overdue exposure tighten working capital and make it harder for firms to protect margins. In Romania, this translates into more volatile profit outlooks. While over one third of businesses expect margins to improve, a similar share anticipates deterioration. This contrasts with CEE, where stability remains the dominant expectation. The lower share of firms expecting no change highlights a more uncertain and less predictable operating environment.

.2026-07-14-09-38-32.png)

Risk perceptions follow a similar pattern. Romanian companies identify economic slowdown and inflation as the main threats to B2B payment behaviour, in line with the wider region. However, concerns about geopolitical instability and regulatory change are more pronounced. This suggests greater exposure to external uncertainty and policy shifts, which can disrupt both demand and payment performance. Risks such as currency volatility, cybersecurity, and fraud play a less central role in Romania. This indicates that firms remain primarily focused on macroeconomic and structural challenges rather than operational risks.

Overall, the data points to a more fragile and less balanced outlook in Romania. While businesses across CEE face similar pressures, Romanian firms operate with greater uncertainty, and higher sensitivity to external shocks, reinforcing the risk of continued strain on payment behaviour and profitability.

For a full overview of the 2026 survey results for Romania, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis