Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Slovenia’s economy shows moderate growth, with activity driven primarily by domestic demand and sustained investment, providing a stable foundation for business operations. However, inflation remains high, continuing to put pressure on corporate costs and margins. External conditions pose an additional challenge, with weaker demand from key export markets weighing on trade performance and creating headwinds for Slovenia’s highly open economy.

Within this context, Slovenian companies are adopting a cautious approach to trade credit. Less than half of business-to-business (B2B) sales are carried out on deferred payment, slightly below the CEE average, although usage is rising, particularly among mid-sized and large construction firms. Across various segments, businesses are extending credit more consistently to sustain demand and protect their position in export-driven supply chains.

Payment policies follow two approaches. Most firms aim to get paid faster by offering shorter terms, while around one third give longer terms to stay competitive. This helps boost sales, but it also puts more pressure on working capital as payments take longer to come in.

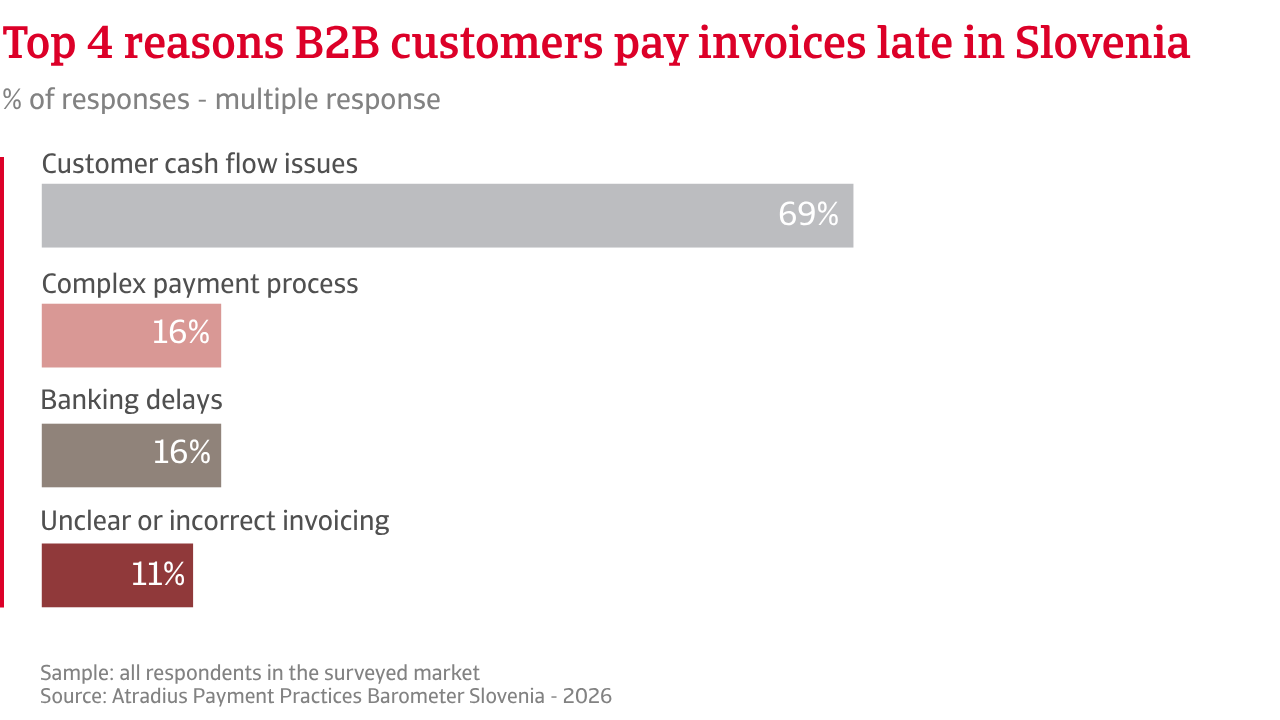

Customer payment behaviour is widespread in Slovenia. More than eight in ten companies, in line with the regional average, face delays from B2B customers, putting pressure on daily cash flow. These delays are not evenly spread. Instead of building slowly, they often worsen quickly once payments are late, making cash flow less stable. This increases the need for tighter credit control. The main cause is customer cash flow pressure, made worse by complex processes and administrative issues. Most firms are managing to collect payments faster, but progress is uneven. Around two in five businesses still face long delays, with payments going well past agreed terms. This leads to steady, ongoing bad debt rather than rare but extreme losses.

This matches the wider trend in insolvencies. Although corporate bankruptcies have trended upward over the past couple of years, they are not cited as the main reason for write-offs. Most losses come from invoices that remain unpaid for too long or from long disputes. Recovery is often low, with many cases ending in little or no repayment, showing weaknesses in how these situations are resolved.

This may explain why cash flow is under strain in Slovenia, but fewer companies say it affects investment or hiring compared with the wider CEE. Most companies are taking a more proactive approach to risk, focusing on improving processes, working more efficiently and using tools like credit insurance, rather than limiting trade.

Overall, Slovenia shows a fragile credit environment. Trade credit remains essential for doing business with B2B customers, but companies need to manage it carefully as they face slower growth, ongoing inflation and higher payment risk.

More than eight in ten companies, in line with the regional average, face delays from B2B customers, putting pressure on daily cash flow.

Almost half of Slovenian firms expect no real change in how B2B customers pay in the coming months. Among those who do expect a change, the outlook is slightly more positive than in much of CEE, with some firms hoping payment behaviour will improve. However, clear pressure remains. Overdue invoices and collection times are still uneven. Payment delays mainly reflect customer cash flow problems, rather than one-off issues. When payments are late, they often get worse quickly, making cash flow harder to manage.

Expectations for insolvencies reinforce this cautious stance. More than four in five businesses expect insolvencies to rise further or stay high. This is very similar to the view across CEE. It shows that companies expect pressure on their customers to continue, rather than improve soon. Only a small number of firms are unsure.

There is, however, a more positive stance on the outlook for profitability. Slovenian firms are more confident than others in the region about improving margins. But this view is not strong. Inflation and rising costs continue to reduce earnings, while late payments tie up cash. Any improvement in margins is likely to be uneven, mainly benefiting firms that manage costs well and collect payments quickly.

When asked about their opinion on the risks that could potentially disrupt B2B payments in the coming months, economic slowdown appears as the main concern, and more businesses in Slovenia highlight it than in the rest of CEE. This reflects the country’s strong link to exports and external demand. Inflation and borrowing costs remain a steady pressure, affecting a similar share of firms as in neighbouring markets. Fewer companies, by contrast, worry about currency volatility or geopolitical risks. This suggests firms see external shocks as more limited.

Overall, businesses in Slovenia expect a payment environment marked by ongoing pressure on cash flow, amid fragile economic conditions, and a disrupted global trade backdrop. Firms indicate that managing liquidity, strengthening risk assessment and improving payment processes will remain central priorities in the months ahead.

For a full overview of the 2026 survey results for Slovenia, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis