Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Switzerland’s business environment is adjusting to a more uncertain macroeconomic cycle, amid expectations of modest GDP growth this year. Geopolitical turmoil, higher energy prices, and an unsettled global trade landscape continue to weigh on confidence. A broad-based surge in corporate insolvencies in recent years, driven by structural pressures and major changes in bankruptcy procedures, has created further challenges for Swiss companies.

This backdrop has coincided with a clear shift in business-to-business (B2B) payment behaviour. 42% of B2B sales in Switzerland now take place on credit, ten percentage points below the Western European average. Companies prefer to preserve liquidity and avoid tying up capital in receivables, contrasting with a broader use of trade credit across Western Europe.

Payment terms in both Switzerland and Western Europe remain within a 30-day credit window. However, Swiss companies, particularly SMEs in trade, more often grant longer terms of up to two months or more. While this approach supports customer relationships, it shifts liquidity risk onto the supplier when settlements slow.

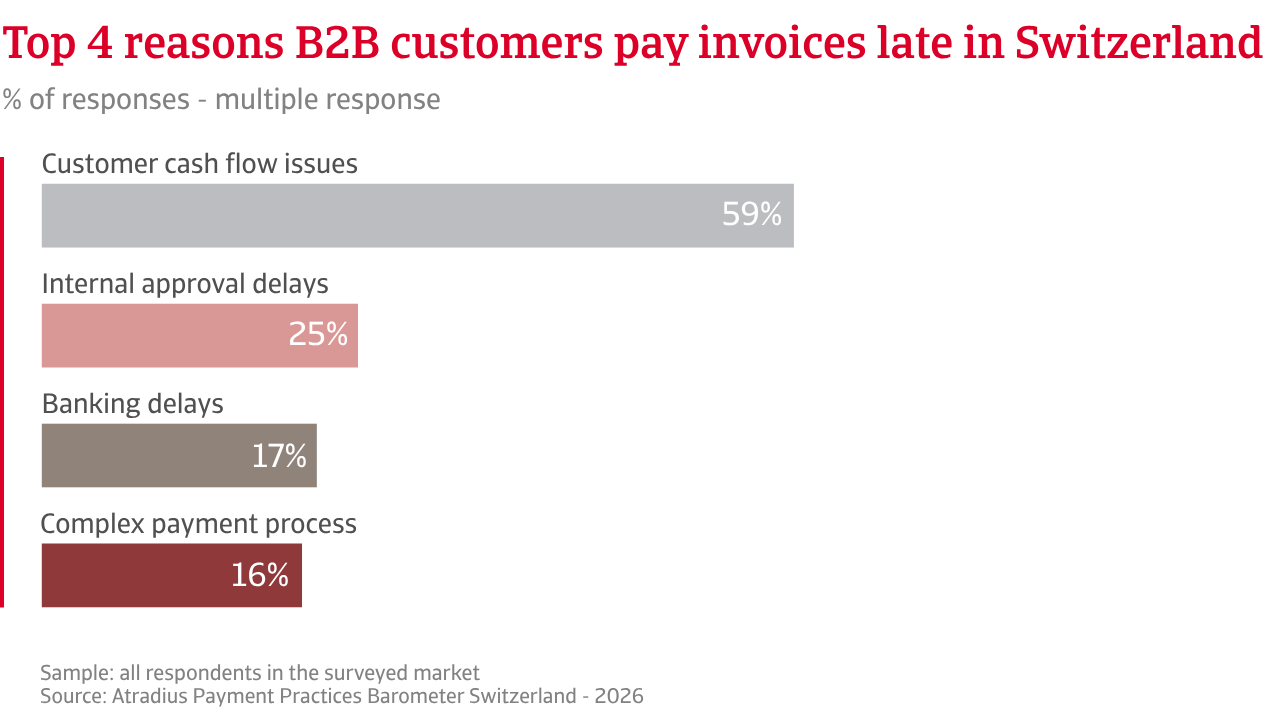

A clear sign that customer payment behaviour has weakened in Switzerland is the sharp rise in slower invoice settlement. At 94%, Switzerland records the highest share of companies reporting late payments across the region where the response rate is 77%. This points to widespread rather than isolated liquidity stress. The impact is strongest in construction, trade, and business services, as they are sectors combining high working capital needs with limited pricing power. Almost one third of B2B invoices issued by Swiss suppliers are now overdue, well above the Western European share of around one quarter. Slower settlement extends cash conversion cycles and pushes Days Sales Outstanding (DSO) higher. Swiss companies therefore face greater exposure to stretched payment cycles than peers in Western Europe, pointing to structurally weaker payment discipline rather than short‑term disruption. This coincides with a higher bad debt risk. Twice as many Swiss firms as those in the region report bad debts clustering around 5% of B2B invoices, indicating that a larger share of receivables becomes uncollectable, eroding working capital, and weighing on profitability.

To mitigate customer payment risk, Swiss firms take a different approach from regional peers, with a higher share of building bad debt reserves, which ties up capital and weighs on profitability, while reducing risk exposure at the point of sale by selling on cash or secured terms. In contrast, far more companies across Western Europe than in Switzerland rely on risk transfer, involving credit insurance, to manage payment risk. This leaves suppliers retaining a larger share of payment risk on their balance sheets, heightening exposure to late payments and bad debts as conditions worsen.

At 94%, Switzerland records the highest share of companies reporting late payments across the region where the response rate is 77%.

Companies in Switzerland tell us they see limited scope for improvement during the year ahead because customer liquidity remains fragile and operational uncertainty continues to cloud financial planning. The best hope is to find some stability during a challenging economic period. Most companies in both Switzerland and Western Europe anticipate that payment behaviour of B2B customers will not change in any meaningful way. The view signals acceptance that the pressures shaping current payment patterns will persist.

Where Swiss businesses stand out is their belief that insolvency levels will not shift significantly in the short term. Most consider the current high levels to be a structural feature of the landscape rather than a short-lived spike. They believe elevated insolvencies will remain part of the operating environment even if growth stabilises. Western European firms are more inclined to expect a further rise in failures, especially in trade. Their more cautious stance reflects weaker economic momentum, persistent cost pressure, and less predictable customer demand. A sizeable number of Swiss and Western European companies express uncertainty about the short-term outlook for insolvencies, which reinforces the impression of a more volatile and demanding backdrop.

Both Swiss and Western European companies foresee little relief on profit margins. They expect subdued demand to continue, coupled with persistent cost pressures that leave little room for improvement. Operating costs remain elevated, while price increases are harder to pass through in a market where customers are cautious and budgets are tightly managed.

A significant finding of our survey is that the most pressing concern for businesses in Switzerland is the uncertain outlook for both the domestic and global economy. This reflects the country’s strong reliance on export markets, many of which are experiencing weaker momentum. Demand from neighbouring euro area economies has softened, and domestic growth shows limited capacity to offset the external drag. Inflation and cost pressures remain part of the Swiss risk mix, but they carry less weight due to the country’s more stable price environment.

Geopolitical instability is an equal worry for Swiss and Western European companies, although the latter feel the cost squeeze more acutely and expect a more unpredictable inflation path in the short term. This highlights the persistent gap between regions, with Switzerland focused on demand weakness and Western Europe more concerned about price pressure. Overall, the picture is of firms operating in an environment that has become more difficult to navigate and in which managing customer credit risk is paramount against a backdrop of heightened economic and trade uncertainty.

For a full overview of the 2026 survey results for Switzerland and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis