Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Across Türkiye, an average of 41% of business-to-business (B2B) sales take place on credit, slightly below the average for CEE. Medium and large businesses in construction and trade drive most of this activity. Survey findings point to a stronger shift towards credit-based B2B trade in Türkiye than in CEE.

Payment terms are notably more relaxed in Türkiye than in the region overall. More companies in Türkiye offer payment terms beyond 30 days. Around 56% grant up to two months from invoicing, compared with 33% in CEE. Terms extending to three months or more are also more common, particularly among large construction firms. This positions Türkiye as the most flexible market in the region. Businesses extend terms to sustain sales and remain competitive.

B2B payment behaviour in Türkiye has worsened in recent months. Businesses reporting delays now outnumber those seeing faster settlement. This indicates rising payment risk and increased pressure on working capital. It contrasts with CEE, where conditions are more supportive, despite some variation across markets.

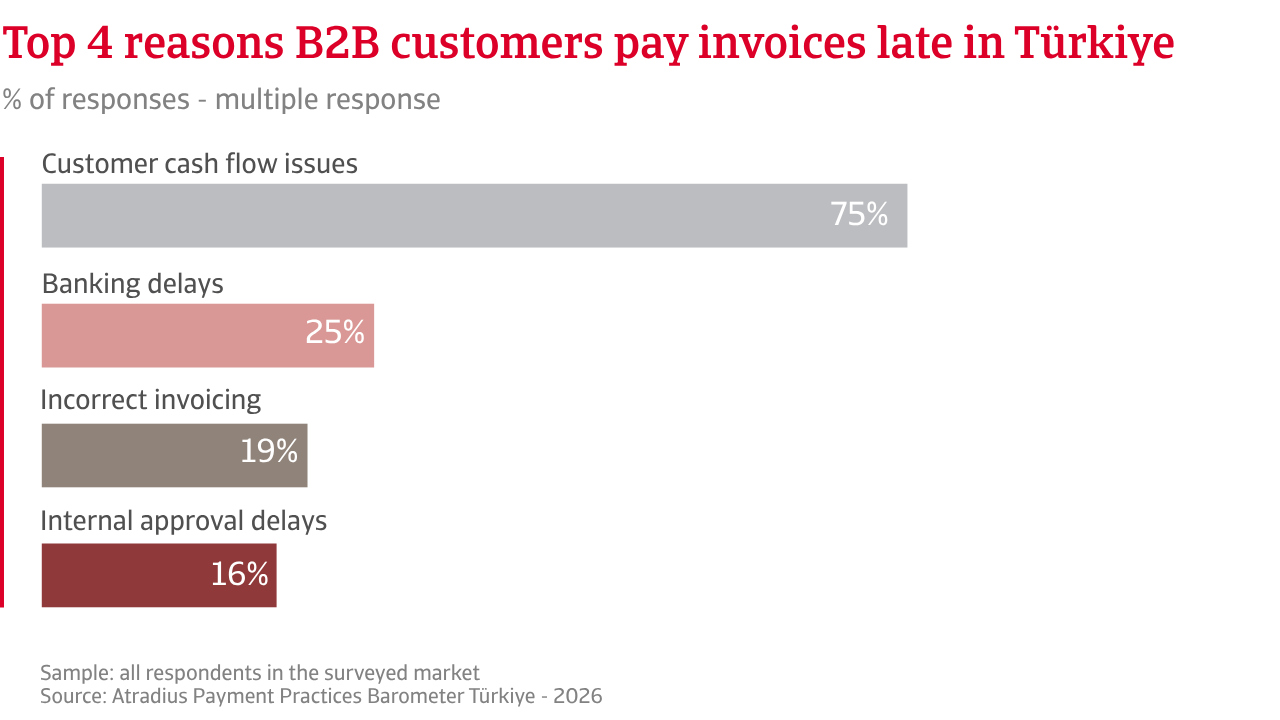

Within this context, 86% of companies in Türkiye report payment delays from customers, with over one third of invoices overdue, above the CEE average. Medium companies in trade are the most affected. The share of overdue invoices has risen further in recent months. This highlights increasing liquidity strain. More than three quarters of businesses cite customer liquidity shortages as the main driver, compared with around three in five in CEE.

Payment collection is also taking longer. Reports of payments collected more than two months late are more frequent in Türkiye. This helps explain the higher likelihood of bad debt write offs. Around one quarter of companies report increasing credit losses. These losses often exceed 5% of receivables. Ageing invoices and unreachable or inactive customers are key causes. The impact is particularly evident among medium-sized firms in construction and trade.

Operational consequences are significant. Around twice as many companies in Türkiye as in CEE report disruption to cash flow planning. Liquidity constraints directly affect day-to-day operations. Businesses rely more heavily on external financing to bridge shortfalls. Many also delay payments to suppliers to preserve liquidity. Fewer companies in CEE report such pressures, pointing to a more stable environment.

To manage these risks, companies in Türkiye prioritise immediate cash protection. They are far more likely to request cash or secured payment. Early payment incentives are also widely used to accelerate inflows. Shorter payment terms are another common response. Credit insurance uptake is higher than in CEE, reflecting increased risk exposure. Overall, businesses focus on protecting liquidity and limiting the impact of delayed payments.

Throughout Türkiye, an average of 41% of business-to-business (B2B) sales take place on credit, slightly below the average for CEE. Medium and large businesses in construction and trade drive most of this activity.

Across both Türkiye and CEE, most businesses do not expect significant short-term changes in B2B payment behaviour. Customer liquidity remains under pressure, shaping a cautious outlook across the region. However, expectations are more negative in Türkiye. A higher share of businesses anticipates a further deterioration in customer payment timings than in CEE, suggesting that current payment risks are not easing and may strengthen in the coming months.

This outlook aligns closely with expectations around insolvency trends. More companies in Türkiye than in CEE believe insolvency levels will rise in the short term, reinforcing concerns about financial weakness and the risk of business failures. At the same time, views are mixed. Some respondents expect insolvency levels to stay elevated rather than increase further, while others report no clear opinion, reflecting ongoing uncertainty about the direction of the economic environment. Overall, the outlook points to continued pressure on payment performance. Türkiye appears more exposed to downside risks, with businesses bracing for further deterioration. In contrast, CEE shows relatively more stability, although challenges remain across the region.

Profit margin expectations remain cautious in Türkiye and across CEE, pointing to a softer profitability outlook. This trend is most evident among SMEs in the trade sector. Rising input costs, slower payment cycles and weaker payment discipline continue to weigh on margins, limiting businesses’ ability to protect profitability. A clear expectations gap emerges between Türkiye and CEE. Turkish companies appear more exposed to margin pressure and persistent uncertainty than their regional peers. In contrast, firms across CEE show greater confidence in their ability to protect profits in the coming months. However, this confidence remains measured rather than strong.

Concern about macroeconomic pressure on B2B payment behaviour is also widespread, with stronger stress signals in Türkiye. Economic slowdown is the leading concern in both Türkiye and CEE, highlighting widespread anxiety about weakening demand and its impact on companies’ ability to pay. Inflation and cost pressures rank second, indicating that rising costs continue to weigh on margins and constrain liquidity.

Beyond these common challenges, Türkiye shows greater exposure to financial instability risks. High levels of concern around currency volatility and interest rate fluctuations point to a more fragile financial environment, where exchange rate movements and higher borrowing costs directly influence payment behaviour. By contrast, businesses in CEE place greater emphasis on geopolitical instability. This reflects a different risk perception, with more focus on external shocks rather than domestic financial volatility.

For a full overview of the 2026 survey results for Türkiye, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis