Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

Companies in Ireland operate in a more balanced business-to-business (B2B) payment environment than many of their Western European peers. An average of 44% of B2B sales are now transacted on credit, which is below the regional benchmark. Irish firms have increased the use of B2B trade credit during recent months, mirroring a broader European upward trend. This reflects the fact that customers are managing liquidity more carefully, prompting suppliers to extend terms to support sales. Competition remains intense, particularly in B2B markets where demand has softened. The modest scale of the increase in trade credit suggests that risk appetite remains disciplined.

Payment terms in Ireland are broadly similar to those in Western Europe, with most companies offering a 30-day credit window. Irish companies, however, are more willing than their peers across the region to extend credit up to two months from invoicing. This reflects a supplier preference to protect long-standing trade relationships. Terms beyond this remain rare in both Ireland and throughout Western Europe.

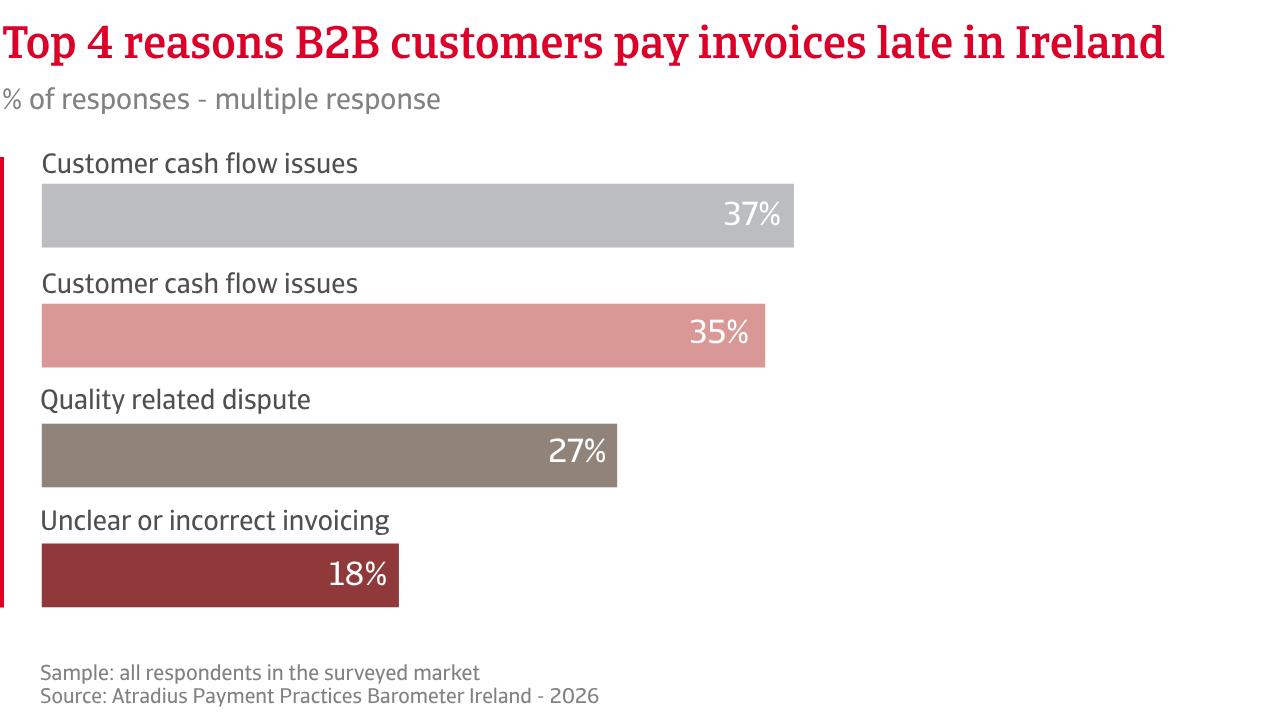

Our survey finds that payment behaviour of B2B customers in Ireland is showing signs of improvement, a marked contrast to the general trend in Western Europe. Overdue levels are easing in Ireland, whereas overdue pressure continues to build across the region, reflecting stronger headwinds affecting customers. The reasons for payment delays also differ. Fewer Irish businesses attribute late payments to customer liquidity shortages than those throughout Western Europe. Delays are instead more often linked to operational factors such as banking processing issues or disputed invoices. Importantly, overdue invoices are typically resolved within the first month past due, keeping Days Sales Outstanding (DSO) broadly aligned with agreed terms.

Credit losses remain contained as most Irish firms report low write-offs, although a meaningful minority face pressure. Stress appears concentrated in specific sectors, rather than being systemic. In Western Europe losses are more widespread, reflecting ongoing strain. Bad debts in Ireland are driven mainly by how long invoices remain overdue. Across the region, customer insolvency plays a more significant role.

Working capital pressure reflects these patterns. The impact of late or non-payment is more contained in Ireland, while companies across Western Europe face broader and more structural strain, which affects financing and operational flexibility. Irish firms prefer to use credit insurance and commercial negotiation to mitigate against customer payment risk. Western European firms rely more heavily on internal buffers, tighter controls, and legal enforcement, which signals more persistent stress.

Irish companies are more willing than their peers across the region to extend credit up to two months from invoicing. This reflects a supplier preference to protect long-standing trade relationships.

Our survey finds that most Irish companies anticipate stability in B2B customer payment behaviour during the months ahead. A minority of businesses are more cautious in their outlook, believing there could be some deterioration. This broadly aligns Ireland with Western Europe, where continuity rather than an improved picture defines business sentiment. The wider macroeconomic backdrop explains this restraint. Ireland’s growth outlook has softened as external demand moderates and global conditions remain uncertain. Inflation weighs on input costs that remain high, while interest rates continue to have an impact on corporate financing. Employment remains resilient, but confidence has fallen slightly, particularly among firms with a domestic focus.

Insolvency expectations reflect this balance. Although most Irish companies do not foresee a significant change in current insolvency levels, which remain contained and broadly steady, more firms in Ireland than in Western Europe expect a short-term increase in insolvencies. This suggests an underlying sensitivity to funding conditions. The remaining companies, with a similar proportion to the regional average, report no clear view, which only reinforces a mood of uncertainty. Construction continues to account for a significantly high share of insolvency instances, reflecting pressure from higher financing costs and softer project pipelines.

There is a divergence of opinion about future profitability between Irish and Western European firms. Although most businesses in both areas do not expect meaningful short-term change, Irish firms express more optimism about rebuilding margins. This stands in contrast to Western Europe, where sentiment focuses on holding the line rather than regaining lost ground. Potential inflation shifts could offer some margin of improvement for Irish companies, even as cost pressure persists. Differences are also evident in assessment of what will drive payment risk. While economic slowdown tops the list of concerns in both Ireland and Western Europe, this is much more pronounced among Irish firms. Inflation and cost pressures follow closely, at similar levels across both markets. This confirms that macroeconomic factors are expected to significantly affect short-term payment risk throughout the region.

The clearest divergence, however, lies in financing conditions. Irish businesses express much stronger concern about borrowing costs, refinancing risk, and exposure to variable rate debt. Cost of money and domestic economic pressure dominate the outlook. By contrast, Western European firms highlight a wider mix of external and structural risks, including regulation, cross border exposure, supply chain disruption, and sector specific downturns. Ireland’s payment risk outlook is therefore shaped primarily by interest rates and growth uncertainty. Western Europe faces a broader risk landscape, driven by regulatory complexity and geopolitical strain. For Irish businesses, B2B payment behavior will be less affected by external shocks and more by the domestic cost of capital.

For a full overview of the 2026 survey results for Ireland and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis