Atradius Atrium

Atrium - für ein vereinfachtes und transparentes Management Ihrer Kreditversicherungspolice. Login Atradius Atrium

Deutschland

Deutschland

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Deutschland

Dänemark

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Norwegen

Österreich

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

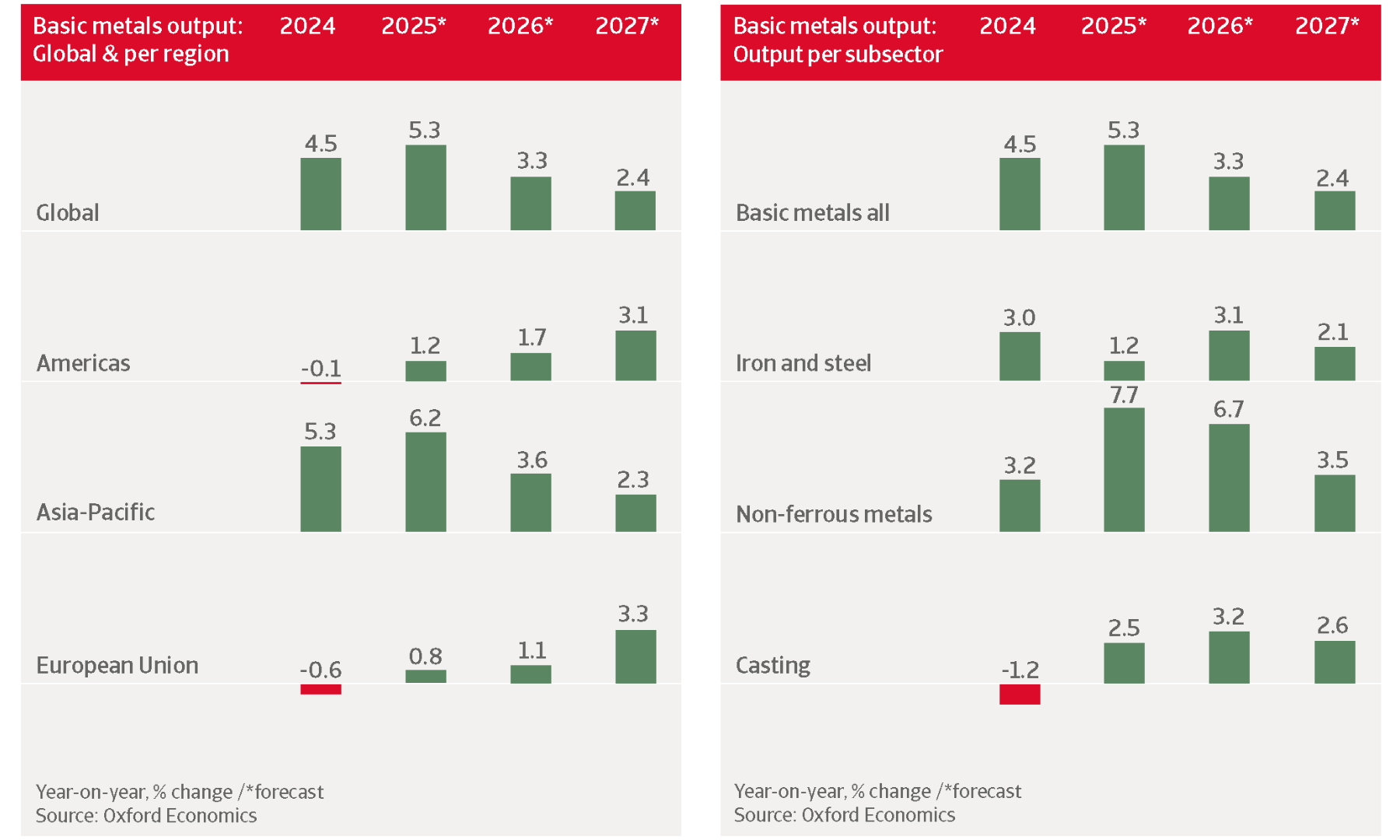

After a 5.3% increase last year, global basic metals production growth is expected to slow down, to 3.3% in 2026 and 2.4% in 2027. In many markets demand from key manufacturing industries has started to decrease, as front-loading activity and tariff implementation delays have subsided. That said, global manufacturing is expected to rise by 2.9% this year, supporting ongoing metals and steel demand.

.2026-03-02-07-34-24.png)

Global iron and steel output is forecast to increase by 3.1% in 2026 and by 2.1% in 2027. Excess capacity is weighing on the segment, and consolidation has been slow. Due to tariffs and sanctions the global steel market is becoming increasingly fractured, and inefficiencies will emerge.

Non-ferrous metals production is expected to increase by 3.5% in 2026 and by 2.9% in 2027, which is above average for the whole basic metals industry. AI-related capital spending and a more growth-friendly US policy mix is underpinning high-tech and capital-goods demand - key consumers of aluminium, copper, and speciality steels.

.2026-03-02-07-35-16.png)

We forecast basic metals production to increase by 2.9% in both 2026 and 2027. Lower interest rates and positive investment incentives due to the One Big Beautiful Bill (OBBA) should pave the way for growth in US manufacturing and related metals and steel demand. However, ongoing trade policy insecurity for businesses and investors is a downside risk for US economic growth.

Due to tariffs US steel producers are gaining market share and additional revenue, but their investment in new production facilities remains limited.

We expect US iron and steel output to grow by 3% in 2026 and 3.3% in 2027. Most domestic iron and steel producers are gaining market share and additional revenue due to higher prices. However, investment in new domestic iron and steel production facilities remains limited, as tariffs could be removed at any point.

Non-ferrous metals production is expected to rise by 3.1% in 2026 and 2.7% in 2027. Aluminium is the largest subsector by volume, and tariffs have pushed prices to record highs. Copper refining has expanded, helped by strong AI and data centre demand.

Energy prices are much lower in the US than in other regions, due to the size of US domestic energy production. Therefore, US metals and steel producers have a competitive advantage over their peers in Europe and Japan.

Credit risk is higher for some small and mid-sized companies, especially those with a leveraged balance sheet and liquidity issues. Businesses that rely on imports have seen higher input costs, which led them to increase prices in order to protect their profit margins.

We expect basic metals output to contract by 4.2% again in 2026 after two years of decreases. The US-imposed 50% tariff is cutting off Canadian steel companies’ main export market and has started to affect sales and profits.

Steel producers are aggressively pursuing cost-cutting measures, and layoffs are occurring. They remain remain exposed to weaker US demand and longer-standing constraints, such as high costs. The credit risk has deteriorated.

Aluminium trade flows from Canada to the US are expected to continue, even as demand will likely weaken due to higher prices.

We expect Chinese basic metals output growth to slow down to 2.5% in 2026 and 1.0% in 2027. This is mainly due to lower steel output. Steel supply exceeds demand, which has put prices and margins under increasing pressure.

Steel producers suffer from the ongoing liquidity woes in the property sector and economic growth slowdown. Export growth offers only limited relief as countries increase trade protectionism against China’s steel exports.

The non-ferrous metals subsector is faring better, as the government prioritises advanced manufacturing, electric vehicles and renewable energy production. This segment is expected to grow by 3.3% this year. However, there are overcapacities in some major segments like aluminium, nickel, and copper.

Credit risk in the Chinese metals and steel sector remains elevated due to the challenging business environment with low prices and margins. In particular in the steel segment some financially weak and smaller players may encounter liquidity issues.

We expect Indian basic metals output to grow by 8.7% in 2026 and by 6.5% in 2027. Demand is driven by robust economic growth. India’s rapid economic progress, urbanisation, and growing population will sustain metals and steel production in the mid to long-term.

India is already the world’s second largest steel and aluminium producer. Substantial new capacity additions are planned across both ferrous and non-ferrous segments over the rest of the decade.

We expect Japanese basic metals output to shrink by 0.4% this year, followed by a 0.7% rebound in 2027. US tariffs and trade policy uncertainty are weighing on exports and investment of key buyer industries like machinery and automotive. About 12% of Japanese exported metal products go to the US.

The automotive sector is a main end-user of Japanese steel and aluminium, and cost pressures are high. Other issues are subdued domestic demand, rising imports—particularly from China—and high reliance on raw materials and energy imports.

In Southeast Asia demand for metals and steel is stable due to growth in housing (construction), ongoing government infrastructure projects and foreign investment in data centres and manufacturing.

Regional production is growing and becoming self-sufficient as it reduces imports. In 2026 gross output of basic metals is expected to grow by 9% in Indonesia, 3% in Singapore, 3% in Thailand, and 9% in Vietnam.

In Southeast Asia´s metals and steel industry capacity expansion meets financial stress. Global oversupply and ongoing price volatility are weighing heavily on margins across the region.

Despite pockets of stable demand, the sector continues to operate under significant pressure. Persistent global oversupply and ongoing price volatility are weighing heavily on margins across the region. At the same time, high capital intensity and elevated debt levels remain a burden, as many producers have taken on additional leverage to fund capacity upgrades and meet the transition toward green‑steel technologies.

Overall, the outlook remains challenging, with financial vulnerability most pronounced among highly leveraged and smaller operators.

After a 0.8% increase in 2025 we expect basic metals output in the EU to grow by 1.1% in 2026. Economic growth remains subdued at 1.0% this year, affected by weaker global demand and ongoing heightened uncertainty.

We expect a gradual recovery of metals performance in H2 of 2026 as past shocks fade and industrial demand rebounds. In 2027 EU basic metals output is forecast to increase by 3.3%.

The Cross Border Adjustment Mechanism (CBAM) definitive period started on 1 January 2026. It raises the cost of importing carbon-intensive metals into the EU by applying a carbon price to foreign basic metals. This removes the cost advantage of higher-emission, non-EU producers and is expected to support EU market share, strengthen domestic pricing power.

Furthermore, the EU has also tightened its steel import restrictions which come into place mid-2026, which should give a further boost to domestic steel producers.

After three years of contraction, we expect German basic metals output to rebound only modestly in 2026, by 0.5%. For quite some time the sector has suffered from weak demand of the key buyer industries automotive, construction, and engineering, while the US import tariffs are a blow to exports.

The credit risk situation of the industry remains strained, as subdued demand, elevated energy costs, and low sales prices have deteriorated margins. Payment delays and insolvencies have increased over the past year, and the situation will remain tense in the coming months. Mainly in focus are automotive suppliers and highly geared companies.

We expect that the recovery gains momentum in H2 of 2026, due to higher economic growth in Germany, as the government's large fiscal stimulus gets underway. New infrastructure investment and higher defence spending should support metals and steel demand. However, planning and implementation delays are likely, while US tariffs and prevailing uncertainty continue to weigh on export opportunities.

While basic metals output is expected to recover by 5.7% in 2027, a full rebound to pre-pandemic levels over the coming years is not on the cards.

We forecast Italian basic metals production to increase by 1.3% in 2026 and 0.5% in 2027. The sector is entering a phase of slight recovery and consolidation, with increasing prices and demand for non-ferrous metals due to energy transition and AI investment.

CBAM measures, stock depletion and increasing demand in Europe should lead to a slight steel segment rebound during the second half of 2026. However, tariffs and a weaker USD make the cost of special steel products and aluminum imported from Italy more expensive for US companies.

Margins of metals and steel businesses have deteriorated in 2025 and are likely to remain under pressure this year due to modest demand, still elevated energy and borrowing costs, and higher raw materials, shipping, and labour costs.

Credit risk in the industry remains high. We are observing longer payment terms and several requests for payment plans, in particular by weaker companies. Metals and steel insolvencies have increased in 2025, and we expect no major improvement in 2026.

Basic metals and steel output are expected to decrease by 8.4% in 2026. This sharp contraction is in part caused by the closure of several blast furnace mills which are being replaced by electric arc furnaces that should come online between late 2026 and early 2028. Another issue is weaker demand due to a slowdown of UK economic growth.

I expect the number of UK metals and steel insolvencies to remain elevated, with heavily-stocked and debt-reliant businesses mainly at risk.

In addition, metals and steel manufacturers and suppliers continue to face unrelenting higher input costs including wages and high debt servicing fees. There is no expectation for significant demand recovery in the near-term. An exception are niche markets such as aerospace alloys and battery metals.

Failures of metals and steel businesses were above historic levels during 2024. These insolvencies were concentrated primarily in the fabricated metals sub-sector. While there was a decrease in 2025, we expect the number of metals and steel insolvencies to remain elevated in 2026.

Mainly at risk are heavily-stocked and debt-reliant businesses vulnerable to further price fluctuations and reliant on expensive debt to support working capital.

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the metals and steel industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Fragen?

Rechtlicher Hinweis