More insolvencies expected in 2022

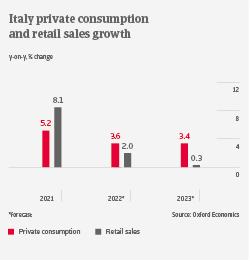

Retail of consumer durables benefited from Italy´s economic recovery in 2021. Private consumption increased by 5.2% and retail sales grew 8.1% (down 7.8% in 2020). The rebound was also driven by public incentives for home renewals and fiscal support for households. Online sales of electronics/small domestic appliances and furniture increased 10% and 18% respectively in 2021. While larger brick-and-mortar retailers are adapting to online competition by launching multichannel sales options, smaller retailers are still less prepared to shift towards online business.

Retail sales growth will slow down to 2% in 2022. This is due to the long life-cycle of larger household appliances and furniture products after the recent sales surge. Following a whopping 20% increase in 2021, we expect domestic appliances value added to contract by 5% this year. Consumer electronics sales will decline after high sales over the past two years and with special events (e.g. high demand for decoders and TVs due to a shift to new digital standards). Another reason for lower consumer durables sales is high inflation (forecast at almost 6% in 2022), driven by sharply increased oil and gas prices. This severely weighs on disposable incomes and discretionary spending. Private consumption growth in 2022 has been revised downwards, from 6% in February to 3.6% currently.

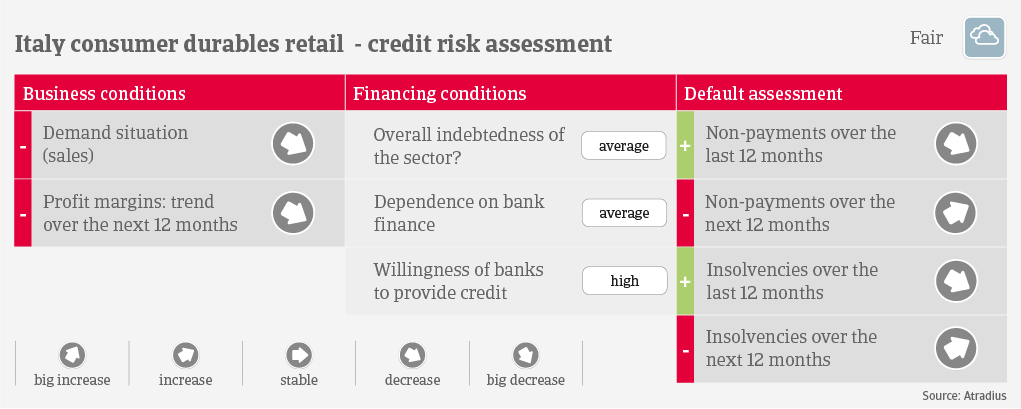

We expect profit margins of consumer durables retailers to decrease in the coming months, as passing on higher production, energy and transport costs to end-consumers will be difficult, given the high competition in the market.

Payments take 60-90 days on average, and the number of payment delays and insolvencies has been low during the past 12 months. However, due to the current challenges, we expect more payment delays and insolvencies in H2 of 2022 and in early 2023, although not a sharp increase.

Our underwriting stance remains neutral for all consumer durables subsectors. Consumer durables retailers´ working capital requirements remain high to sustain purchases and maintain an adequate level of inventories. A main criterion for us is the capability of businesses to manage recourse to financial debt adequately in relation to their working capital requirements.