More difficult market conditions after robust growth in 2021

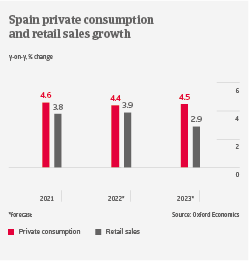

The Spanish consumer durables market grew strongly in 2021 as the economy rebounded from the Covid-related recession in 2020. Household appliances and small electrical items sales increased 14% and 8% respectively. Furniture sales rose 11%, while consumer electronics grew 3.5% (after a 7.5% increase in 2020). Online sales of consumer durables increased a whopping 60% in 2020, followed by a 3.7% growth last year. Currently e-commerce accounts for about 30% of sector sales, and brick-and-mortar retailers have increasingly set-up their own online sales channels.

Retail sales growth has started to slow down since H2 of 2021, due to rising inflationary pressures and supply chain bottlenecks. Those bottlenecks will remain an issue across all consumer durables subsectors in the coming months, while we expect annual inflation to increase by more than 6% this year, as gas, fuel, electricity and food prices have sharply risen during the past couple of months. Lower household purchasing power negatively affects discretionary spending this year. We expect domestic appliances value added to contract 5% in 2022 after growing 7.5% in 2021. Additionally, both brick-and-mortar and online retailers face higher transport cost as well as increased producer prices passed on by manufacturers. Due to strong competition in the market, retailers can only partly pass on those costs to end-customers.

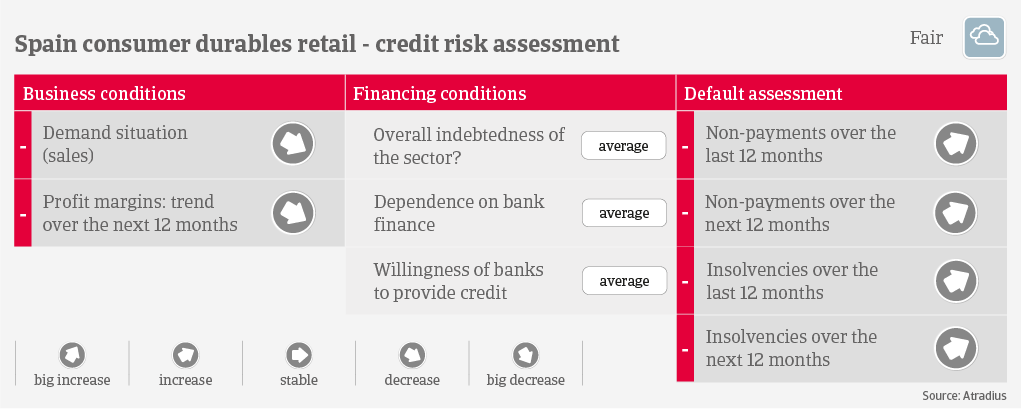

Lower demand and higher costs negatively affect revenues and profit margins of businesses, which should lead to deteriorating payment behaviour in the coming months. In Q1 of 2022, insolvencies of retailers (food and non-food) grew 7.8% year-on-year, and we expect further increases in the coming twelve months. The number of business failures and the amount of claims will be highly impacted by inflation development in the coming months and its impact on future discretionary spending. On a positive note, fiscal support of domestic consumption is still ongoing, and the government has taken measures to curb energy price inflation.

Our underwriting stance is neutral for all consumer durables retail subsectors. While exposed to rising consumer prices and soaring costs for raw materials, energy and transport, the sector is still quite resilient compared to other industries.