Ongoing, but lower sales growth in 2022

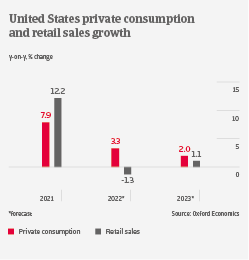

We expect that consumer durables sales should continue to grow in 2022, as higher wages and house prices support ongoing demand. However, growth will slow down compared to 2021, because with the lifting of social distancing measures there is high pent-up demand of non-durable goods and services. Additionally, high inflation, driven by gas and food prices, will impact discretionary spending. We expect domestic appliances output to contract 2.5%, after a whopping 12.2% increase in 2022. Furniture and consumer electronics revenues should grow 3.5% and 2.8% respectively, but remain impacted by supply bottlenecks and shipping delays. Online sales accounted for about 23% of total retail sales and are forecast to grow between 11% and 13% this year.

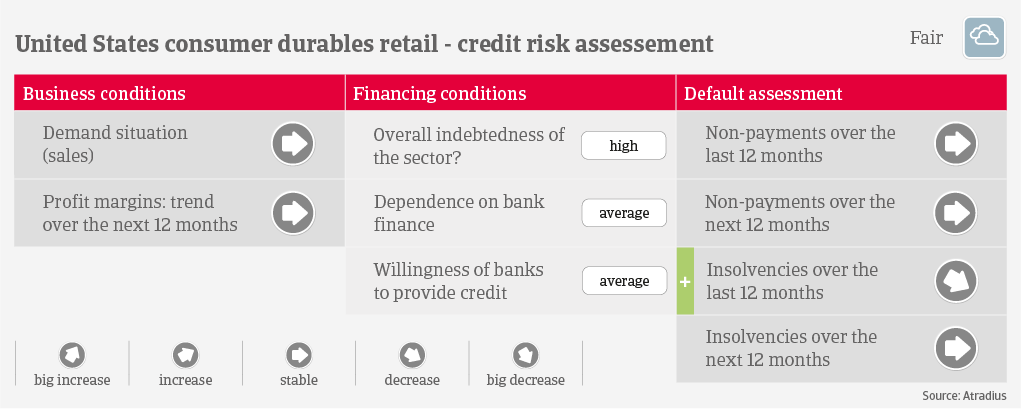

Retailers´ profit margins have increased in 2021, helped by pandemic-related cost savings, and we expect them to remain stable in the coming months. The current cost inflation should have a lagged effect on businesses´ financials, and retailers are able to pass on a share of increased input costs to end-customers.

Payments in the industry take about 60 days on average. As retailers have returned to normal operations after the height of the pandemic, payment trends should remain stable. In 2021, US retail bankruptcies decreased to the lowest number seen during the past ten years. This was due to buoyant sales, fuelled by government stimulus for consumers. Additionally, consumer durable retailers benefited from business liquidity support programmes like the Paycheck Protection Program (PPP), while low interest rates provided favourable funding opportunities for debt refinancing. We expect no substantial increase in retail bankruptcies in the coming twelve months, given the ongoing sales growth.

However, there are downside risks for the credit risk of smaller retailers. Many of them have to increase lending because PPP loans are no longer available, while at the same time banks are more reluctant to provide loans to this business segment. As interest rates rise, smaller retailers are more susceptible to financial distress if their liquidity shrinks. Additionally, ongoing supply chain bottlenecks and the impact of persistently high inflation on consumer sentiment remain downside risks in the coming months.